With stock valuations elevated after such a strong first half, earnings growth will be key to holding, or potentially building on these gains. LPL Research believes stocks have gotten a bit over their skis, but earnings season may not be the catalyst for a pullback in the near term given all signs point to another solid earnings season and stocks have mostly performed well during the peak weeks of reporting season in recent years. We may not get an increase in second-half estimates over the next couple of months — that’s a lot to ask — but we should get a few points of upside and double-digit earnings growth for the second quarter on the back of technology strength.

RETURN TO DOUBLE DIGITS

Earnings season is right around the corner, with the big banks — JPMorgan Chase (JPM), Citigroup (C), and Wells Fargo (WFC) — scheduled to report on July 12. With the consensus expectations currently calling for a 9% increase in S&P 500 earnings per share (EPS), a double digit gain for the first time since the fourth quarter of 2021 looks highly likely. That’s the main headline, but the sub-headline is the composition of that earnings growth.

EXPECT DOUBLE-DIGIT EARNINGS GROWTH IN THE SECOND QUARTER

Source: LPL Research, FactSet 06/27/24

Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly.

Estimates may not materialize as predicted and are subject to change.

Last quarter the “Fab 5” consisting of Alphabet (GOOG/L), Amazon (AMZN), Meta (META), Microsoft (MSFT), and NVIDIA (NVDA), drove 7.8 points of S&P 500 EPS growth, which was actually slightly more than the rest of the index (“the 495”). In other words, those five companies drove all of the S&P 500’s earnings growth and earnings for the 495 were just shy of flat.

Turning to this quarter, the contribution from mega cap technology will be big again, but we should start to see some contribution from the rest of the market. Based on current estimates, the “Super Six” is expected to drive 4.8 points of S&P 500 earnings growth. (We added back AAPL for its expected return to earnings growth in the second quarter, while we leave out Tesla (TSLA) from the original Magnificent Seven because of its more than 30% expected earnings decline.)

This leaves about four points of S&P 500 EPS growth from the rest of the index, which will likely come from healthcare, financials, energy, and utilities. The reversal in healthcare and energy earnings is a big reason why tech will get some help. Healthcare sector earnings fell 25% year over year in the first quarter, in large part due to losses absorbed from acquisitions by Bristol Myers Squibb (BMY). This quarter, the sector is expected to grow earnings by nearly 17%. Energy should be able to stage a similar turnaround, with consensus estimates calling for a 13% year-over-year earnings increase in the second quarter after a 26% decline in the first quarter.

REASONS TO EXPECT GOOD NUMBERS

It won’t take much upside to get to double-digit earnings gains, but there are several reasons to expect a few percentage points of upside, which is typical:

- Estimates have been resilient. S&P 500 companies in aggregate generated four percentage points of upside in the first quarter despite the big healthcare drags to get to that final increase of over 7%. Estimates dipped heading into last quarter’s results, by 2.5%, and we’ve seen the same again this quarter, though not as much (from 9% to 8.8%). While resilient estimates raise the bar and make it harder to clear, they also point to analysts’ confidence in the underlying earnings power of corporate America, a confidence we share. Earnings misses are rare (less than 1 in 10), but without cracks in estimates, we believe an overall earnings miss is even more improbable.

- Steady economic activity. Disinflation is getting most of the attention — and probably justifiably so — given the impact on consumer spending and interest rates. But economic activity in the second quarter rose steadily based on several metrics. The Atlanta Federal Reserve’s GDPNow tracker points to 2.2% second quarter gross domestic product (GDP) growth. The U.S. ISM Services Index jumped more than four points in May to near 54, firmly in an expansion territory, and most of the U.S. economy is services-based.

- Asian export activity bodes well for technology. Historically, S&P 500 earnings growth and Korean export activity have been well correlated. With the rise of Taiwan Semiconductor (TSM) as a key chip supplier, we watch economic data out of Taiwan as well. A lot of technology equipment sold by U.S. companies globally has key supply hubs in Asia. Korean exports to the U.S. rose 25% in April year over year (YoY) and 15.6% YoY in May. Taiwan’s exports to the U.S. rose 80% year over year in April before cooling to a still huge 36% increase in May.

However, there are also several reasons upside may be less than recent trends. First, the strong U.S. dollar will clip foreign earnings for U.S. multinationals by a percentage point or so. Second, the ISM Manufacturing Index, which has also correlated well with earnings, remains below the 50-breakpoint marking expansion. And third, the economic surprise indexes we follow, from Citi and Bloomberg, have both been sliding, suggesting managements’ guidance last quarter may have assumed better economic conditions.

EARNINGS SEASON AS A CATALYST

One of the most difficult questions to answer about earnings seasons is whether results will be a catalyst for stock market gains. For answers to tough questions, we turn to the data.

Our bias remains that a pullback is overdue, and we would recommend investors not chase this rally but rather wait for a dip to buy. That said, based on the data, the next six weeks of earnings results may not offer that opportunity.

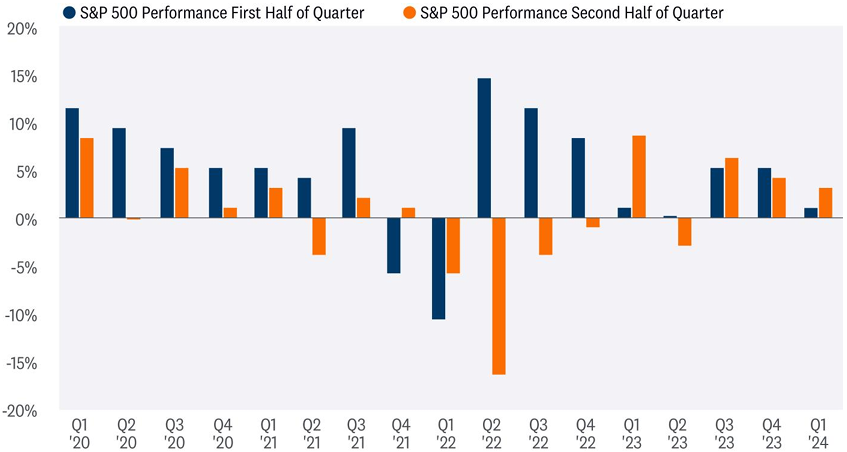

As illustrated in the chart below, in recent years, stocks have done better during the heart of earnings season (from quarter end through the middle of the next month) than they have during the off weeks. We understand some companies report outside of this window, including NVDA, but to keep the time frames equal and keep the analysis simple, we split quarters into halves. Since 2020, the S&P 500 has gained an average of 4% during the first half of the quarter when the bulk of earnings are released, compared to flat average performance during the second half of the quarter when fewer companies report.

So while our expectation is for stocks to pull back at some point this summer, this analysis suggests a dip may not emerge until August after most of the earnings news is reflected in stock prices.

STOCKS HAVE GENERALLY DONE BETTER DURING THE EARNINGS-HEAVY HALF OF THE QUARTER

Source: LPL Research, FactSet 06/26/24

Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly. Estimates may not materialize as predicted and are subject to change.

AS ALWAYS, IT’S ALL ABOUT GUIDANCE

We write this every quarter, but we will watch company guidance closely throughout earnings season to help us gauge just how much earnings growth corporate America might be able to produce in the back half of 2024.

It cannot be overstated how rare it is for estimates to be so resilient this long (again, perhaps a 1 in 10 type of occurrence). Estimates usually fall short of reality at economic inflection points, such as when the economy emerges from recession. This time is different. We’re well past the COVID-19 rebound and even the pause in the economy in 2022. Something different is going on this time, and it is artificial intelligence (AI).

So, given a steady, but not spectacular, economy and continued investment in AI, executives are unlikely to cut their outlooks much, if at all. Pressures have started to build on consumers — remember, we heard from several restaurants last quarter about pushback on high prices and Walmart (WMT) and Target (TGT) cutting prices. We’ll probably get some more of that capping estimates, but we would expect the AI binge and technology strength to keep estimates well supported overall.

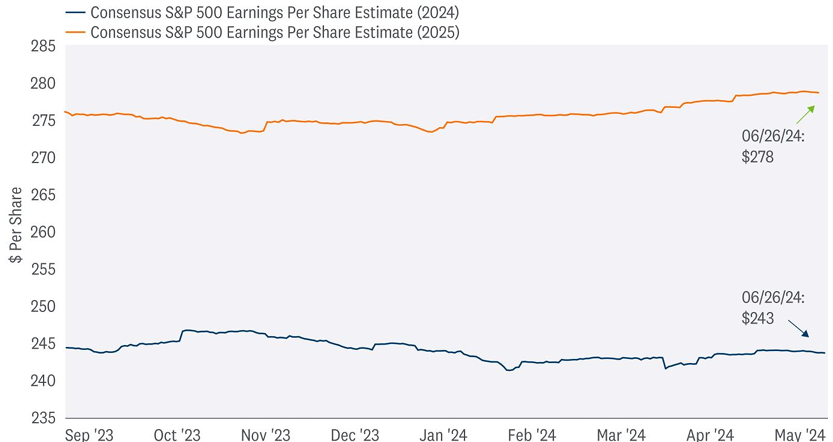

That leads to our 2024 and 2025 estimates, which we will raise in our 2024 Midyear Outlook publication, due out on July 9 (estimates currently sit at $235 and $250, respectively, both reflecting growth in the mid-to-high single digits). Over the next year, earnings growth rates are expected to get a boost from a resilient but slowing economy, AI investment, and easy comparisons in the healthcare and natural resources areas.

2024 AND 2025 CONSENSUS EARNINGS ESTIMATES CONTINUE TO DRIFT HIGHER

Source: LPL Research, FactSet 06/27/24

Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly.

Estimates may not materialize as predicted and are subject to change.

ASSET ALLOCATION INSIGHTS

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities amid the market’s AI enthusiasm, solid earnings trends, and strong technical momentum. However, we would not chase this rally, and prefer to wait for a dip before considering adding to equity allocations. With valuations for stocks elevated and bonds offering more attractive yields, we believe the risk-reward trade-off for bonds is slightly more attractive than that of stocks. More volatility is likely over the balance of 2024 as the economy potentially slows.

Within equities, the STAAC continues to favor a tilt in the Tactical Asset Allocation (TAA) toward domestic over international, with a preference for Japan among developed markets, and an underweight position in emerging markets (EM). The Committee recommends a very modest tilt toward growth style after reducing its overweight position in mid-March. Finally, the STAAC continues to recommend a modest overweight to fixed income, funded from cash.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time.

The prices of small cap stocks are generally more volatile than large cap stocks.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. LPL Financial does not provide investment banking services and does not engage in initial public offerings or merger and acquisition activities.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

RES-000151700624W | For Public Use | Tracking # 597324 (Exp. 07/2025)